Home Insurance

What information is required to obtain a preliminary home insurance quote?

What is included in the home insurance?

What is not included in the home insurance? (can be added for an extra charge)

Dwelling

Private Structures

Personal Property

Loss of use

Personal Liability

Medical Payments to others

Back Up of Sewers, Drains, and Sump

Particular expensive personal property (rings, furs, guns...)

Mold coverage

Flood ( it is a separate policy, not an endorsement)

t.t.

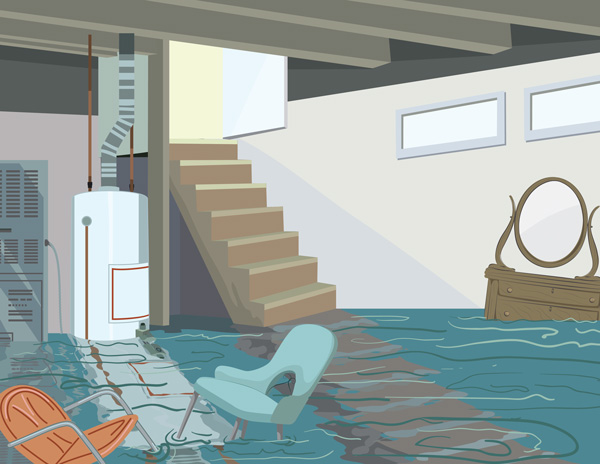

We want to pay more attention to claims due to water

Water is a very slippery thing that can cause unwanted damage and put you under financial burden.

Without an endorsement, normal home owners insurance does not cover damage from direct contact with water

that results from a sudden and accidental discharge, eruption, overflow or release of water from within any portion of:

plumbing system located on the residence premises;

sump pump well or sump pump located on the residence premises;

any system on the residence premises designed to remove or drain sub surface water away from residence premises;

and is a water - reverse flow; or

is from below the surface of the ground whether natural or otherwise.

When home insurance covers water damage?

Home insurance covers water damage only when unexpected water bursts from the water supply and then there is coverage for all electrical connected to it: dishwashers, washing machines, etc. Your home insurance also covers water damage when it occurs due to a storm, for example when the storm tears off the roof and water gets inside (very limited coverage).

Sewer and drain does not cover flood losses. Flood is a separate policy which is mandatory only to certain locations that are marked as a flood zones. Despite this fact, anyone definitely can get a flood policy as well.

What is the solution?

Backed up sewers & drains can wreak havoc on a home, causing thousands of dollars of damage to floors, walls, furniture and electrical systems.

This coverage premium depends on the amount you want to insure and if you want to insure the whole property or only specific appliances and food.

Žodynėlis

Coverage - apdrauda.

Insured - apdraustasis.

Deductible - nuostolių suma, kurią turite sumokėti Jūs. Kuo mažesnis deductible, tuo didesnė draudimo kaina.

Dwelling - namo atstatymo kaina.

Private Structures - apdrauda, skirta atskirų, prie namo neprijungtų struktūrų atstatymui, taisymui atlyginti (pavyzdžiui garažo).

Personal Property - suma, skirta atlyginti namuose esančių jūsų asmeninių daiktų nuostoliams: baldams, buitinei technikai, rūbams ir pnš. Į šią sumą neįeina: vertingi papuošalai, kailiai, meno kūriniai.(Jiems apsaugoti reikalinga papildoma apdrauda.)

Loss of use - suma, kurią išleisite kito būsto nuomai, kol bus atstatyti Jūsų namai.

Personal Liability - apdrauda, kuri dengia dėl tavo kaltės padarytos žalos išlaidas. Viskas, kas įvyko jūsų atsakomybėje - yra personal liability. Galioja visame pasaulyje.

Medical Payments to others - suma, kuri dengia Jūsų namų teritorijoje susižeidusiojo medicinines išlaidas.

Building Code Upgrade and Demolition Costs - bulding code - procentali suma, kuri dengia kainų skirtumą nuo dabartinės rinkos namo atstatymo ir tos, kuri buvo, kai namas buvo originaliai pastatytas.

Identity Theft and Credit Protection - apdrauda, kuri kompensuoja išlaidas, kurias patirsite, jei bus pavogta Jūsų tapatybė, pavyzdžiui: samdysite advokatą, norėdami susigrąžinti reputaciją.

Back Up of Sewers, Drains, and Sump - apdrauda, kuri kompensuoja išlaidas patirtas apsėmus namus, prakiurus vamzdynui, bet tai NĖRA potvynio draudimas.